Saving up and buying a home can be a major undertaking these days with how high home prices are across Metro Vancouver and the BC region.

That’s why it’s important to know the minimum down payment options in BC, so you can get an understanding of how much to save before you’re ready to buy.

By the end of this article, you’ll know how to calculate the minimum down payment, what to consider with down payment percentages, and more!

Check out our other guide on down payments for condos, if you’re looking to buy a condo.

Table of Contents

What is the minimum down payment in British Columbia?

In British Columbia specifically, the minimum down payment when purchasing a home depends on the purchase price of the property, and if you’ll be using it as a principal residence or investment property.

Principal Residence

The minimum down payment when purchasing a principal residence depends on the purchase price as follows:

Calculation: For homes priced at $500,000 or less

A minimum down payment of 5% of the purchase price is required.

For example, let’s say you’re purchasing a studio apartment in Langley, BC for $450,000. The minimum down payment required for this property would be $22,500. This is 5% of $450k.

Calculation: For homes priced between $500,001 and $999,999

The minimum down payment is 5% of the first $500,000 plus 10% of the portion of the purchase price above $500,000.

Let’s say you’re purchasing a 2 bedroom Condo in Burnaby, BC for $870,000. The minimum down required to buy this property would be $62,000.

This is broken down by $25,000 from 5% of the first $500,000, and then $37,000 from the 10% of the remaining $370,000.

Calculation: For homes priced at $1 million or more

A minimum down payment of 20% of the purchase price is required when purchasing a home of $1,000,000 or more. With how high BC home prices are, this can be common for many home buyers if you’re looking to purchase in the Metro Vancouver area.

Let’s say you’re looking to buy a 4 bedroom detached home in East Vancouver for $1,800,000. The required minimum down payment would be $360,000.

These requirements are consistent across Canada, too.

Investment Property

If you’re purchasing an investment property in BC, one that you won’t live in as your primary residence, the minimum down payment is 20% of the total purchase price.

Calculation: Buying a condo investment property in Burnaby

Let’s say you’re looking to purchase that same condo in Burnaby as the previous example, for $870,000. If it’s an investment property, your minimum down payment required would be $174,000.

Additional Costs When Buying to Consider

When buying a home, you not only have to come up with the down payment, but there are other closing costs and expenses you’ll need to consider, too. One of the major expenses is Property Transfer Taxes (PTT).

Learn more about PTT and how it applies to home buyers in BC.

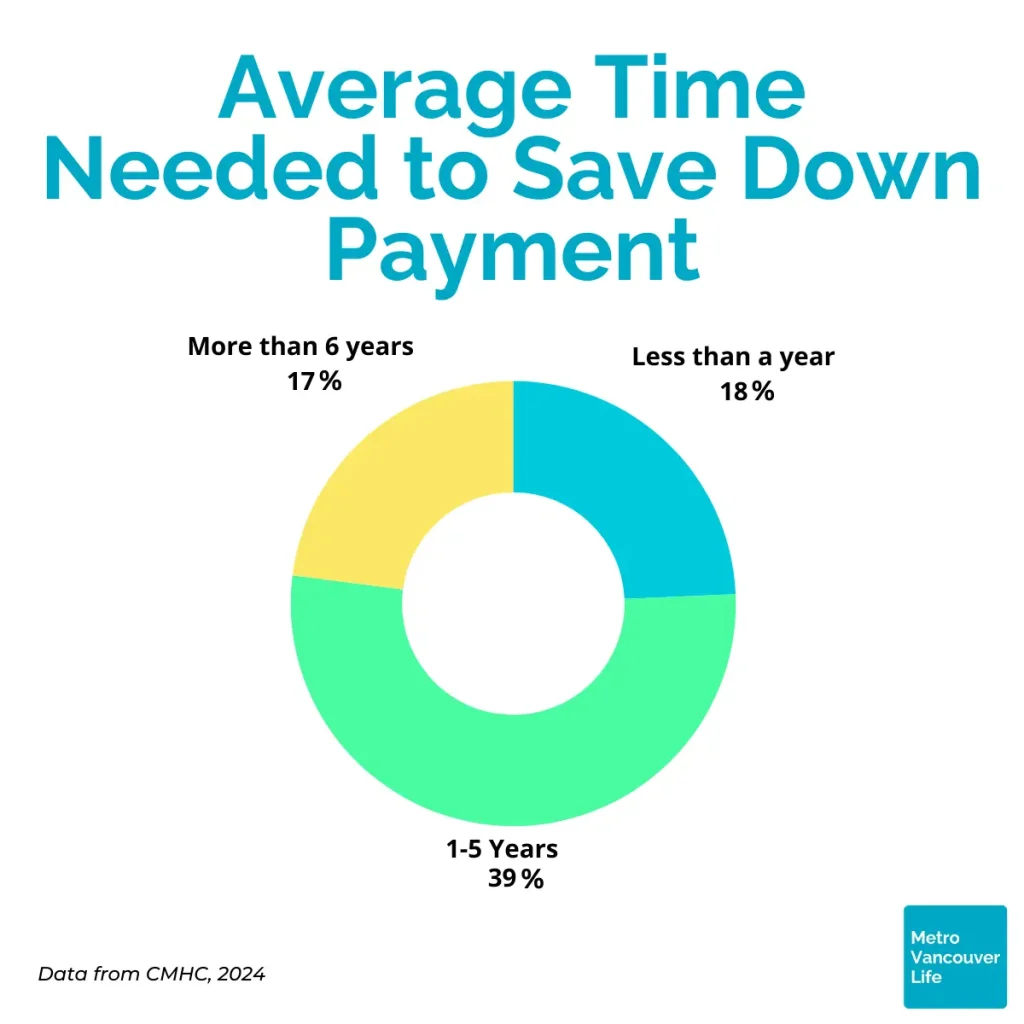

What’s the typical time to save for a down payment?

According to research done by CMHC in 2024, the typical time it takes for people to save for a down payment is about 4.2 years. Ranging from less than a year to over 6 years.

How much do people typically put down on a house?

How much people put down on a property comes down typically to their specific financial situation.

Some people may opt to put more of their available funds towards the down payment so they have a smaller mortgage payment each month. While others may opt for the minimum down payment so they can get into the market quicker than waiting and saving for those higher down payments amounts.

Typically, a 20% down payment is the target for home buyers. This ensures that you’ve put enough money down on the property that you won’t have to pay for mortgage insurance.

However, many first-time home buyers may opt to put down the minimum or near the minimum down payment to get into the market.

That’s why, we highly recommend connecting with a reliable mortgage broker. They’ll help you understand your options by providing you with analysis and recommendations of what may work best for your financial situation. We have reliable people we can recommend if you reach out to us.

How much is Mortgage Insurance for a Minimum Down Payment?

Mortgage Insurance for a minimum down payment is typically 4% of your mortgage amount. For example, if you’re buying a house and only put down the minimum down payment allowed in BC, you’ll need to pay extra for Mortgage Insurance.

For a $750,000 home, the minimum down payment is $50,000. This is calculated as 5% of the first $500,000 ($25,000) plus 10% of the remaining $250,000 ($25,000).

With this minimum down payment, you’d need to borrow $700,000 from the bank. The mortgage insurance on this loan would be about 4% of the loan amount, which is $28,000.

This $28,000 for insurance doesn’t have to be paid all at once. Usually, it gets added to your mortgage, so you pay it off little by little each month with your regular mortgage payments.

While this does make the monthly payments a bit higher, it allows you to buy a property without coming up with the full 20% or $150,000 for a $750,000 purchase price, in this example.

If you want to find out more, check out this CMHC fact sheet on Mortgage Insurance.

Benefits and Drawbacks of Different Down Payment Amounts

Benefits of Larger Down Payments (20% or More)

A larger down payment offers a few advantages to home buyers, especially when it reaches 20% or more of the home’s purchase price. One main benefit is avoiding mortgage insurance, such as CMHC Mortgage Loan Insurance in Canada, which can save you thousands of dollars over the life of your loan. Additionally, with a larger down payment, the loan principal is reduced, leading to lower monthly mortgage payments.

Starting with more equity in your home provides a financial buffer against market fluctuations, offering greater stability and peace of mind.

Drawbacks of Larger Down Payments

Larger down payments are not always beneficial, depending on your certain situation.. Saving for such a large down payment like 20% to 25% can be difficult and might delay your ability to enter the housing market.

Another potential drawback is reduced financial flexibility. Allocating the majority of your savings to a down payment may limit your ability to invest in other opportunities or respond to unexpected financial emergencies, like a special assessment on a strata.

Understanding these trade-offs can help you make an informed decision about the right down payment amount for your situation.

Recommended Reading: Choosing To Buy Re-Sale or Pre-Construction Property in BC

Is a Down Payment the Same as a Deposit?

In short, no, the down payment and deposit are not the same thing.

While they are closely related, the deposit is a smaller amount, typically a portion of the down payment that is required to make an offer on a home.

In BC and Metro Vancouver, the standard deposit is 5% of the purchase price of the home. However, this can change depending on the terms you and the seller agree upon.

So, typically, once you’ve submitted an offer and it’s accepted, your Realtor will coordinate getting your deposit and holding that money in trust by the brokerage. This deposit amount is a portion of your down payment. When it comes time to finalize the transaction, that’s when you provide the rest of your down payment to the lawyers or notary.

For example, if you’re putting a minimum down payment of 5% on the value of a $495,000 home, the total down payment would be $24,750. So, a serious deposit may be around $15,000 to $20,000.

Down Payment Assistance Programs

While the province of BC doesn’t have specific down payment assistance programs for residences, it’s important to note that there are several federal programs set up to help Canadians save for a down payment efficiently. These include programs like:

- First Home Savings Account (FHSA)

- Home Buyers’ Plan (HBP)

- And more…

Learn more about first-time home buyers incentives and programs in our guide: Top First Time Home Buyer Programs For BC Buyers.

Can I use money gifted to me as part of my down payment?

In short, yes, you can use money gifted to you as part of your deposit or down payment. Your mortgage broker will want to verify where this gift came from and who it came from, but it’s now a common part of the process.

Gifts for down payments from family have been increasing over the years, as home prices in Metro Vancouver and the rest of Canada soar higher.

According to research by the CMHC, approximately 30% of home buyers in BC received their down payment as a gift amount. And the average gift was approximately $77,000.

Recommended Reading: Understanding Leasehold vs Freehold Property in British Columbia

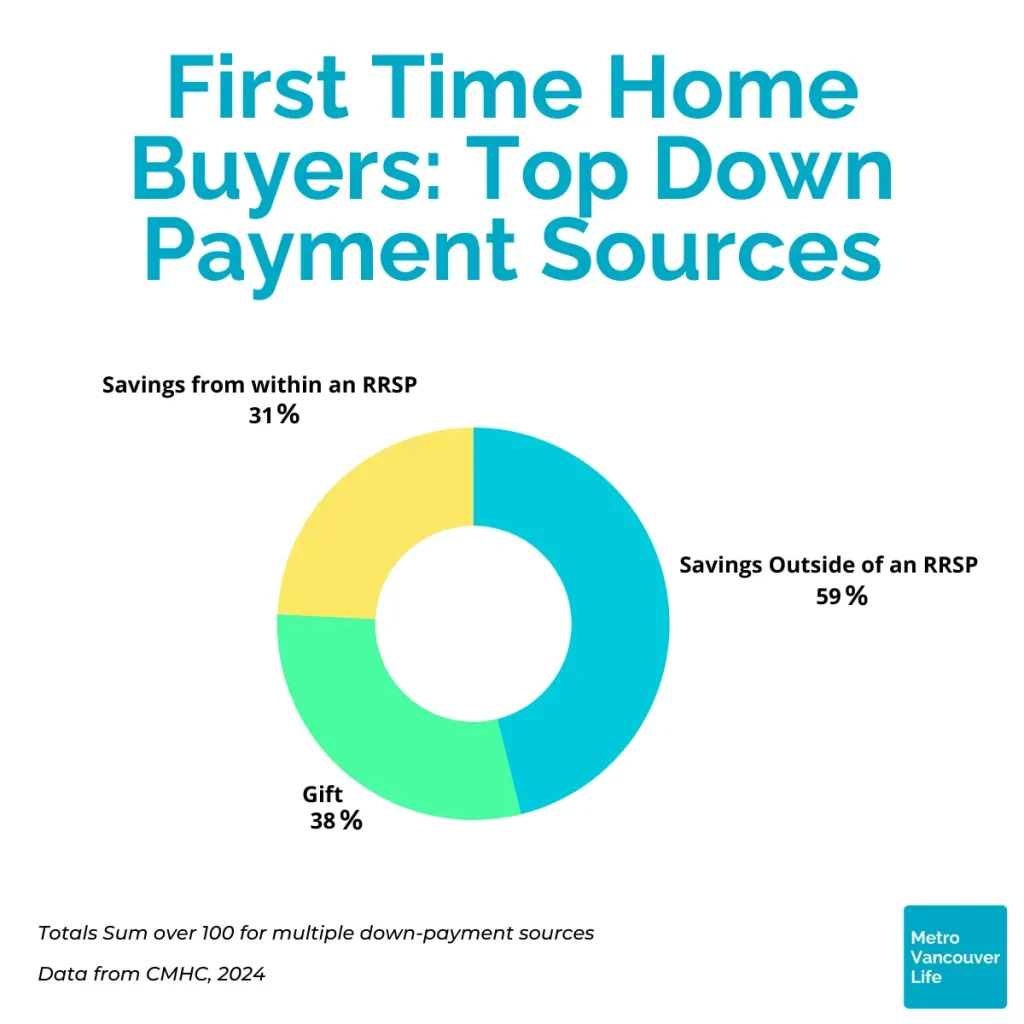

What are common sources of a down payment for a home?

There are usually 4 to 5 common sources of a down payment when buying a home. While a large portion of home buyers work for their money, save, and then buy, common sources can include a mix of:

- Savings outside an RRSP;

- RRSP savings;

- Gifts;

- Equity from current home.

Final Thoughts

Saving for a home is a major first step into your home purchasing journey. The minimum down payment amounts will help guide you on how much you should have saved before you’re able to buy.

And working with a reliable mortgage broker and Realtor will help you navigate your next steps in securing financing and placing an offer just that much easier.

If you’re curious about getting your home buying journey started, don’t hesitate to reach out and contact us today.